In today’s update, we cover several new developments that impact your agency’s pension plans:

• CalPERS’ investment performance for the FYE 06/30/2025.

• How to estimate its impact on your unfunded pension liability.

• Discount rate review process update.

Also, keep reading to the end to find out about the big change happening in this year’s actuarial reports.

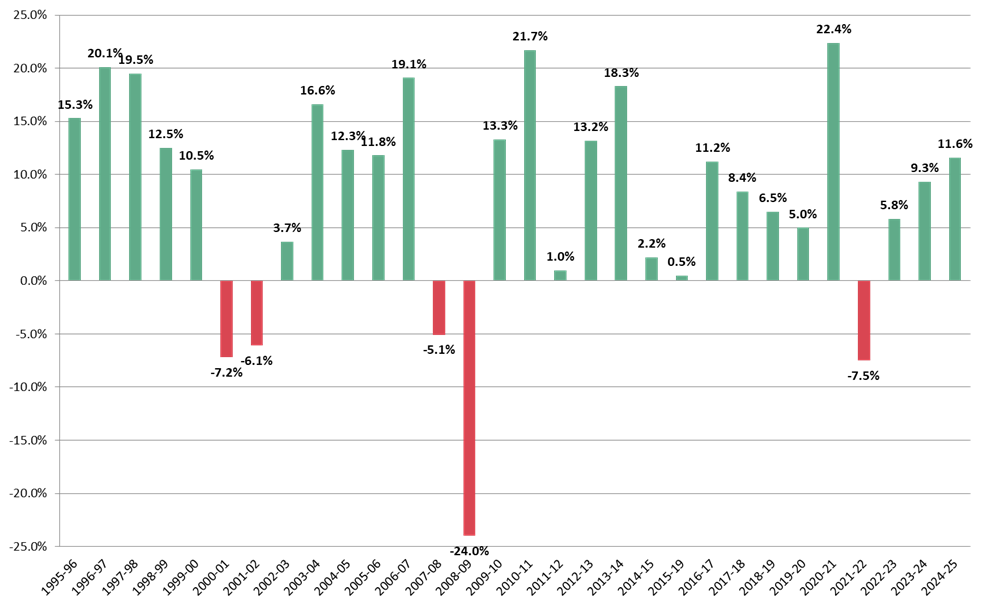

On July 14, 2025, the California Public Employees’ Retirement System (CalPERS) announced a preliminary 11.6% investment return for FY2025. With the second year of strong performance, this is welcome news for many public agencies.

UPDATE: In November 2026, the FY2025 investment return was finalized at 12.1%.

As a reminder, investment performance exceeding CalPERS’ 6.8% target (also known as the discount rate) helps reduce your agency’s unfunded accrued liability (UAL).

The 11.6% investment return for FY 2025 translates into 4.8% of excess earnings over the 6.8% discount rate. This helps lower UAL balances and reduce UAL payments for California public employers. Official impacts will be reflected in the FY2025 actuarial reports, to be published in summer of 2026.

The 30-year history of CalPERS investment returns is shown in the graph below.

With FY 2025 investment return exceeding the 6.8% target, the pension system’s funded status increased from approximately 75% to 78%.

This performance was driven by strong gains in public equities (16.8%), private equity (14.3%), and private debt (12.8%). Fixed income delivered a solid 6.5% return, while real assets posted a more modest 2.7% gain. It should be noted that returns from private equity, private debt, and real assets typically lag by a quarter and remain subject to future adjustments.

To quantify what the 11.6% investment return means for your agency, it is important to understand CalPERS’ funding math.

• For CalPERS to stay on track and avoid significant UAL increases, it needs to average 6.8% in annual investment returns. This target is called the discount rate – the minimum average rate of return that CalPERS needs to achieve in perpetuity so that its member agencies could meet their retirement obligations to employees, retirees, and other beneficiaries.

• Every time that CalPERS misses this target, additional UAL is created.

• However, when investment returns exceed the target (like it did this year), the UAL is reduced.

To estimate the FY2025 excess return impact on your UAL, you can multiply the market value of assets within your pension plan by the 4.8% excess earnings. That will be the approximate amount by which the UAL will be reduced.

For each $1 million in pension plan assets, roughly $48,000 of existing UAL will be removed from each agency’s account.

These lower UAL balances will first be reflected in the 2025 actuarial reports, which CalPERS will publish in July/August of 2026.

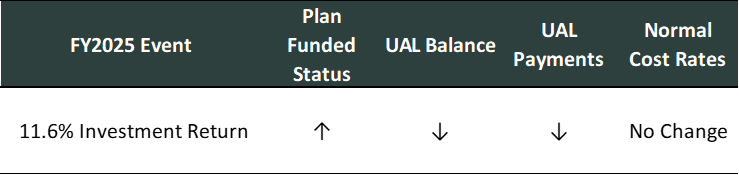

The FY2025 performance will result in higher funded status of pension plans, lower UAL balances, and lower future UAL payments, as the effect of the excess earnings will be spread over the next two decades. There should be no change to the Normal Cost contribution rates due to the investment performance.

The impacts of the FY2025 investment performance are illustrated below:

If CalPERS continues to follow its current amortization practices, the FY2025 UAL reduction will be phased-in over a 20-year period starting with FY2028, with a five-year credit ramp-up:

• The 2028 UAL credit will be 20% of the full annual credit amount

• The 2029 UAL credit will be 40% of the full annual credit amount

• The 2030 UAL credit will be 60% of the full annual credit amount

• The 2031 UAL credit will be 80% of the full annual credit amount

• Only in 2032 will the UAL credit be fully phased-in and continue at that level for 15 more years

Years with excess returns should be allowed to work in your agency’s favor. Unlike UAL increases, which create negative amortization, unamortized UAL credits create additional investment income for your agency's pension account. Thus, maintaining the ramp-up structure for credits can help maximize long-term benefits.

For now, CalPERS elected to pause automatic discount rate reductions in years with excess investment returns. Instead, the Board of Administration is now required to review whether the discount rate should be reduced in the future. With the on-going Asset Liability Management process, any changes to the discount rate are expected to be announced in November 2025.

CalPERS’ average annual returns currently stand at

• 8% over the past 5 years

• 7.1% over the past 10 years

• 6.7% over the past 20 years

These results generally support maintaining the current 6.8% discount rate.

Besides investment-related UAL changes, CalPERS conducts an annual reconciliation comparing actual plan experience to actuarial assumptions. This analysis will result in additional UAL adjustments for FY2025, but we will find out about them only in July/August of 2026.

The actuarial reports for FY2024 are about to land in your MyCalPERS portal. You will notice a big change to how the pension system reports on your pension plans. While Miscellaneous and Safety plans remain separate, CalPERS has decided to consolidate reporting for the Classic and PEPRA plans.

Starting this year, you will only see one report where there used to be two. CalPERS implemented this consolidation to simplify reporting and improve administrative efficiency. However, extra effort will be necessary if you want to separate the Classic and PEPRA data.

Ridgeline Municipal Strategies, LLC can help you evaluate the impacts of the FY2025 investment performance on your pension costs, make sense of the new actuarial report format, and implement appropriate pension cost optimization and mitigation strategies.

Ridgeline's assessment of CalPERS' FY2024 investment performance and its impact on the CalPERS member agencies.

Read this post.webp)

Fire station and apparatus financing is complex. Here we explore the 8 most common financing mistakes made by fire departments.

Read this post

Fire mitigation fees help fire departments get funding for new facilities and apparatus. Ridgeline’s best practices guide shows how to plan, implement, and manage fire mitigation fees for maximum impact.

Read this post

Ridgeline served as a municipal advisor on the issuance of the $10,925,000 Water Revenue Certificates of Participation with $12,000,000 in proceeds for the Tehachapi-Cummings County Water District.

Read this post